New Roof Depreciation Life

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

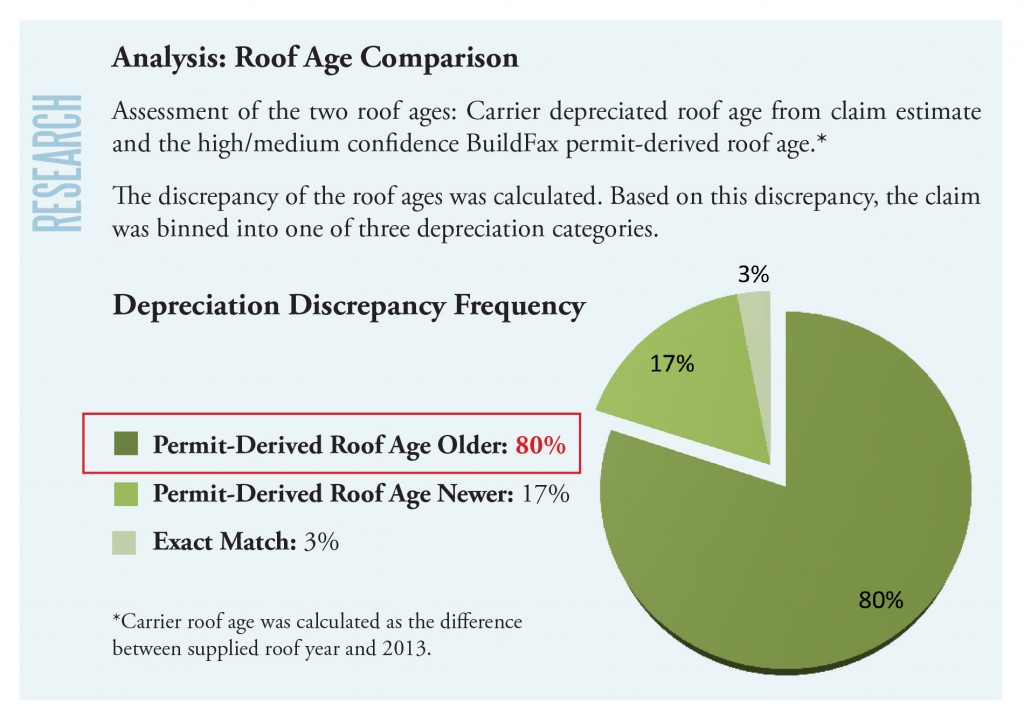

Part Three The Value Of Accurate Roof Age In Claims

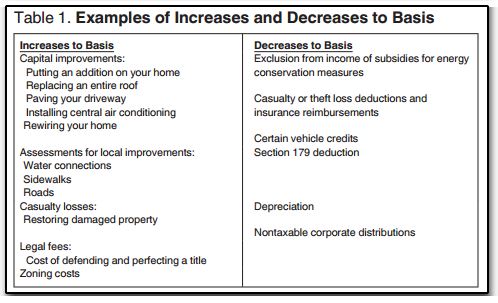

12762 Increasing Basis On An Asset Being Depreciated

What Is The Depreciation Of The Roof On A Commercial Building

Pin On Articles Tips

Section 179d Tax Deduction For Commercial Roof Replacements

Your deductible is 1 000.

New roof depreciation life.

Qualified Leasehold Improvement Property Depre Calculation

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

Understanding Taxes Series Part 1 Depreciation Adventures In Cre

Rv Depreciation What You Can Expect With A New Rv Purchase Used Rvs Rv Life Rv Stuff

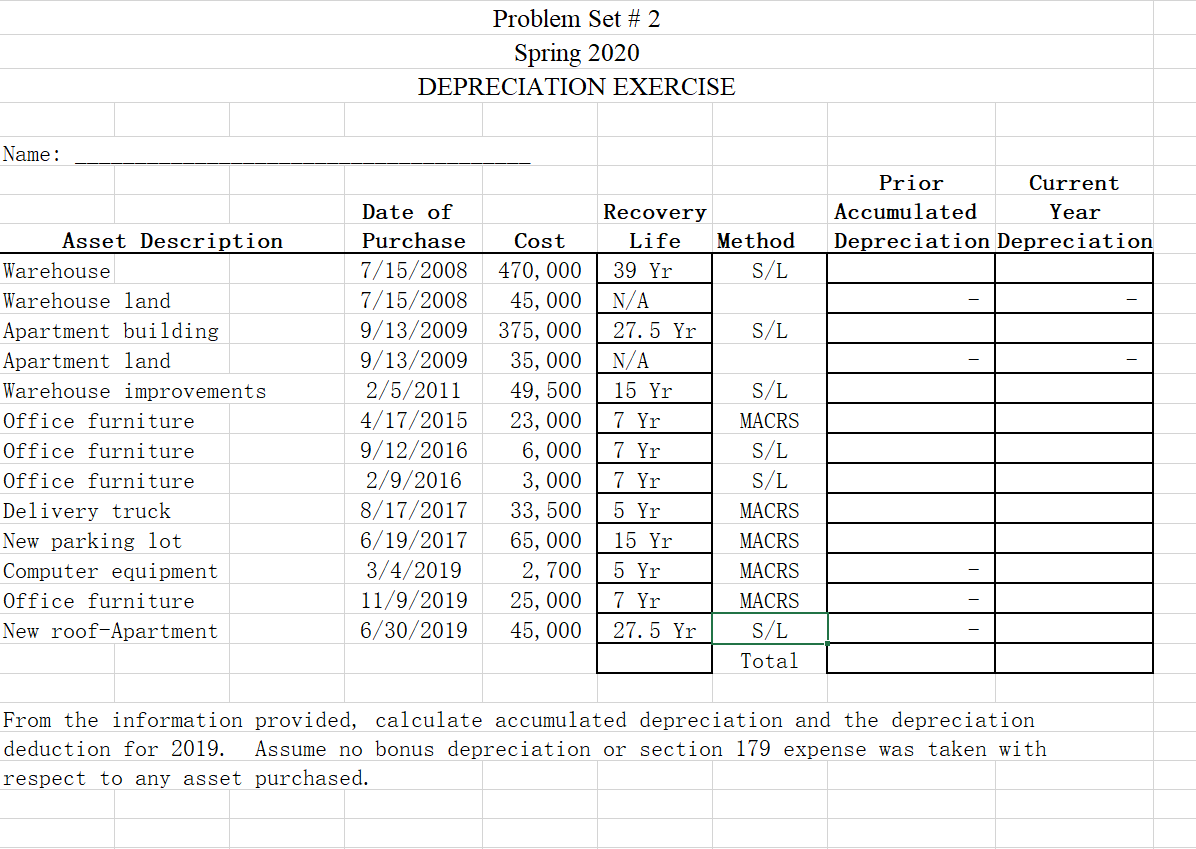

Problem Set 2 Spring 2020 Depreciation Exercise Chegg Com

Tax Depreciation Schedules Australia One Of The Least Benefit Of Property Depreciation Is That They Are Non Cash Deductions It Means Tax Deduction Legal Rule

What Comes First The Property Or The Loan White Paint House House Painting Buying Property

Nonresidential Building Improvements Post 1993 Depre Calc

Real Estate Tax Depreciation Basics Millionacres

E Tax Depreciation Schedule Australia Will Be Australia S Driving Firm Who Give The Best Expense Devaluation Administrat Tax Investing Tax Deductions

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Prateek Grand City Bharosa Jyada Prateek Ka Vaada With Images Property Valuation Melbourne City

Home Based Business Jobs 2269 20180912135821 49 Home Office Tax Deduction Depreciation Recapture Rate 2016 Home Decor Pictures Home Decor Cool Landscapes

Accounting For Equipment And Depreciation Self Progress Accounting Online Courses With Certificates Online Courses

Pin Di Destinasi

Tokens Of Depreciation Instagram Tree House Outdoor

Accumulated Depreciation Meaning Accounting And More In 2020 Financial Management Accounting Principles Fixed Asset

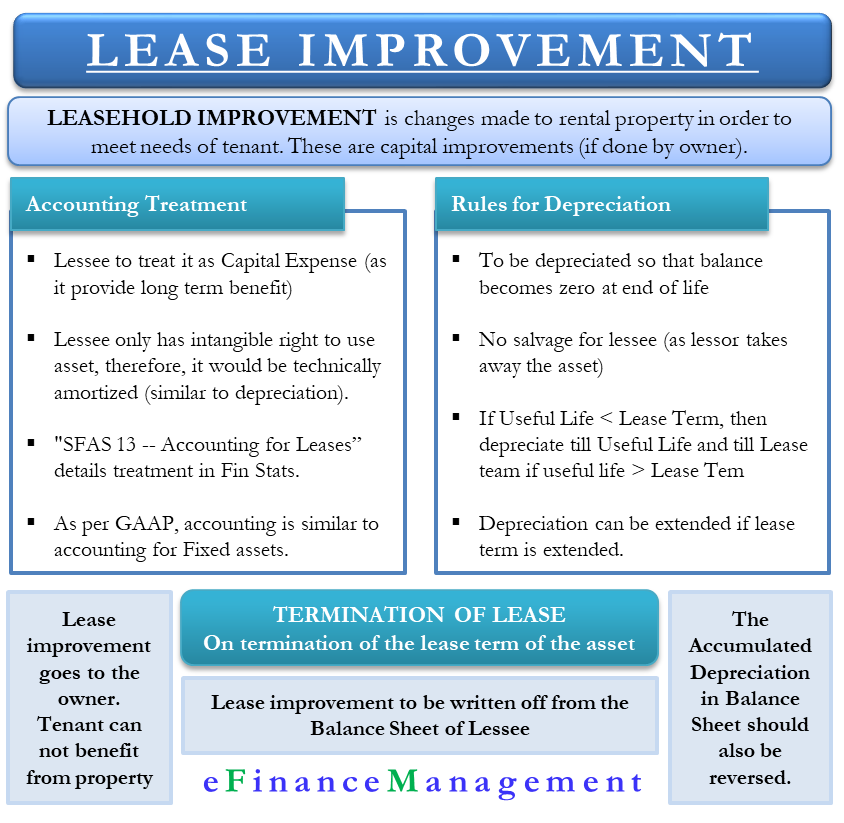

Leasehold Improvement Gaap Accounting Depreciation Write Off Efm

The Information Below Was Provided By Nrel National Renewable Energy Laboratory Download The Pdf Here National Storage System Battery Storage Federal Taxes

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

Balance Sheet Example Template Format Balance Sheet Template Balance Sheet Financial Statement

Xactimate And Insurance Prices Change Every Month Do You Know How Much Www Overheadandprofit Com Insurance Xa American Family Insurance Roofing Fire Damage

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

Home Business Franchise 220 20180912121508 49 Michigan Licensed Beverage Association Members Freedom Filer Home Business 5 16 Home Business Freedom Filer

Source : pinterest.com